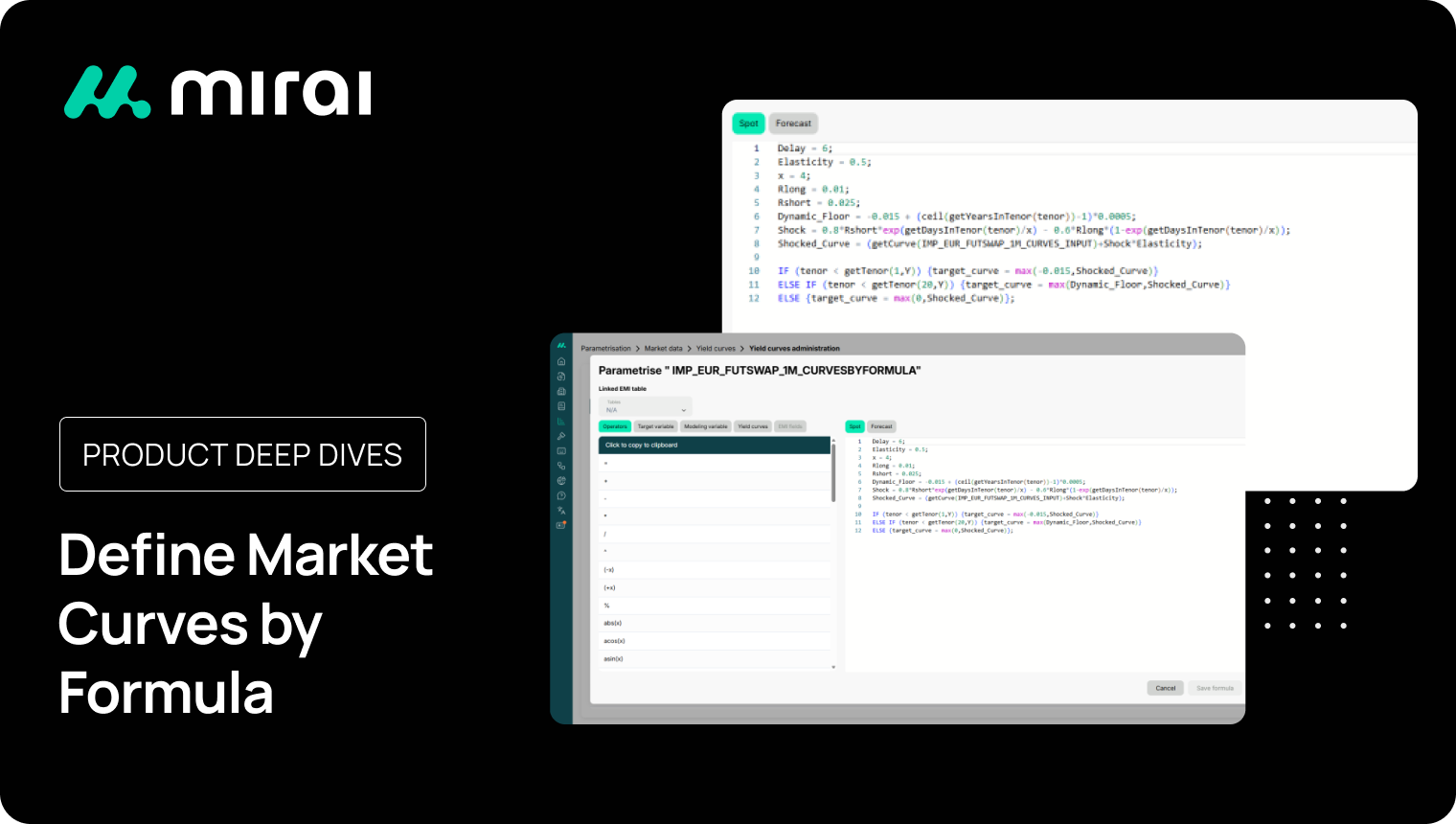

Curves by Formula is a new development that lets you build spot and forecast yield curves directly in the formula editor, so you can automate shocks, encode business rules, and drop repetitive template uploads altogether. You can also reference existing curves inside your formula and even layer multiple sources to build new complex rate indices custom to your business. Mirai will then unify their tenor structures in the resulting curve, so complex designs stay maintainable and consistent across scenarios.

What is it and where to find it

Curves by Formula adds a new formula builder option to curve construction. You work in the same formula builder used for behavioral modeling in Mirai, but with target_curve as the target variable and curve‑specific modeling variables. You can reference standard curves inside your formula, or reference EMI tables that can include external data such as credit spreads or macro rates.

Why it matters

You keep curves in one governed place (the editor), reuse the logic across scenarios, and, when you need a shocked variant, you simply overwrite the formula in the scenario. No spreadsheets, no side files, no re loading of daily templates.

Use Cases

Automated CSRBB credit spread curves from external EMI files

Define CSRBB curves by combining risk free market curves already in Mirai with credit spreads maintained externally in EMI tables. Spreads, shocks, and segmentation (by rating, sector, currency, or maturity bucket) are stored once in an EMI file—often sourced from internal credit models, or regulatory specifications—and referenced directly inside the curve formula.

Using Curves by Formula, the curve builder programmatically adds these EMI based credit spreads to the underlying risk free curve, producing fully consistent credit adjusted spot and forecast curves. Scenario shocks (e.g. widening/narrowing by rating or tenor) are applied by simply switching or overwriting the referenced EMI tables in the scenario, without duplicating curves or loading new templates. This approach automates CSRBB curve construction, ensures alignment between risk free and credit components, and allows large scenario sets to be generated transparently and consistently from governed inputs.

Non‑parallel steepener with a maturity‑dependent floor

Encode an IRRBB style steepener with a floor that starts at −150 bps at immediate maturity and increases by 3 bps per year, reaching 0% by 50 years. Implement the floor with Min/Max around the base curve in spot, then let auto forecast propagate the effect into forwards using your curve’s own interpolation, capitalization, and accrual settings. Shocks remain formula driven and reusable, not one off overwrites.

Final overview

Curves by Formula elevates curve building from a file-loading chore to a governed modeling step. You define spot/forecast once, reference standard curves, enrich EMI‐based attributes, and reuse the logic across scenarios, overwriting formulas when you need scenario specific variants. With dedicated operators, auto forwards, tenor unification, and refined day count handling, Mirai delivers accurate, transparent, and scalable curve generation without templates or manual post-processing.